https://www.zerohedge.com/political/trump-must-avoid-these-3-civilization-killers-when-tackling-national-debt

An Analysis of Daily Events that Impact Your Money

Tuesday, May 27, 2025

Saturday, May 24, 2025

Monday Morning Chartology--early

5/26/25

I

am off on a two and half week vacation in Europe. Be back on 6/16. Enjoy your

Memorial Day weekend.

The Market

Technical

Not a great week for the S&P. Between the

latest Trump tariff tantrum and the disappointedly, fiscally irresponsible Big,

Beautiful Bill, neither stock nor bond investors were very happy. The index

ended the week having broken the uptrend off its April 7th low and

hanging precariously above its 100 and 200 DMAs. The only thing to do now is

see whether the S&P will regain that uptrend or reset those two DMAs. If

the latter, then the next visible support level is the 50 DMA (~5584). Follow

through.

As I noted above, the long bond didn’t fare any

better than the S&P. It pushed through (1) the lower boundary of its very short

term trading range---resetting it to a downtrend and (2) the lower boundary of

its intermediate term downtrend. That leaves TLT in downtrends across all time frames

and below all DMAs. If the bond vigilantes are getting serious about refusing to

go along with these spendthrift morons in the ruling class, expect more

downside.

https://www.zerohedge.com/the-market-ear/end-era-8-incredible-charts-bond-markets

Watch the Japanese long bond.

https://www.zerohedge.com/the-market-ear/want-know-where-markets-go-next-watch-japans-long-bond

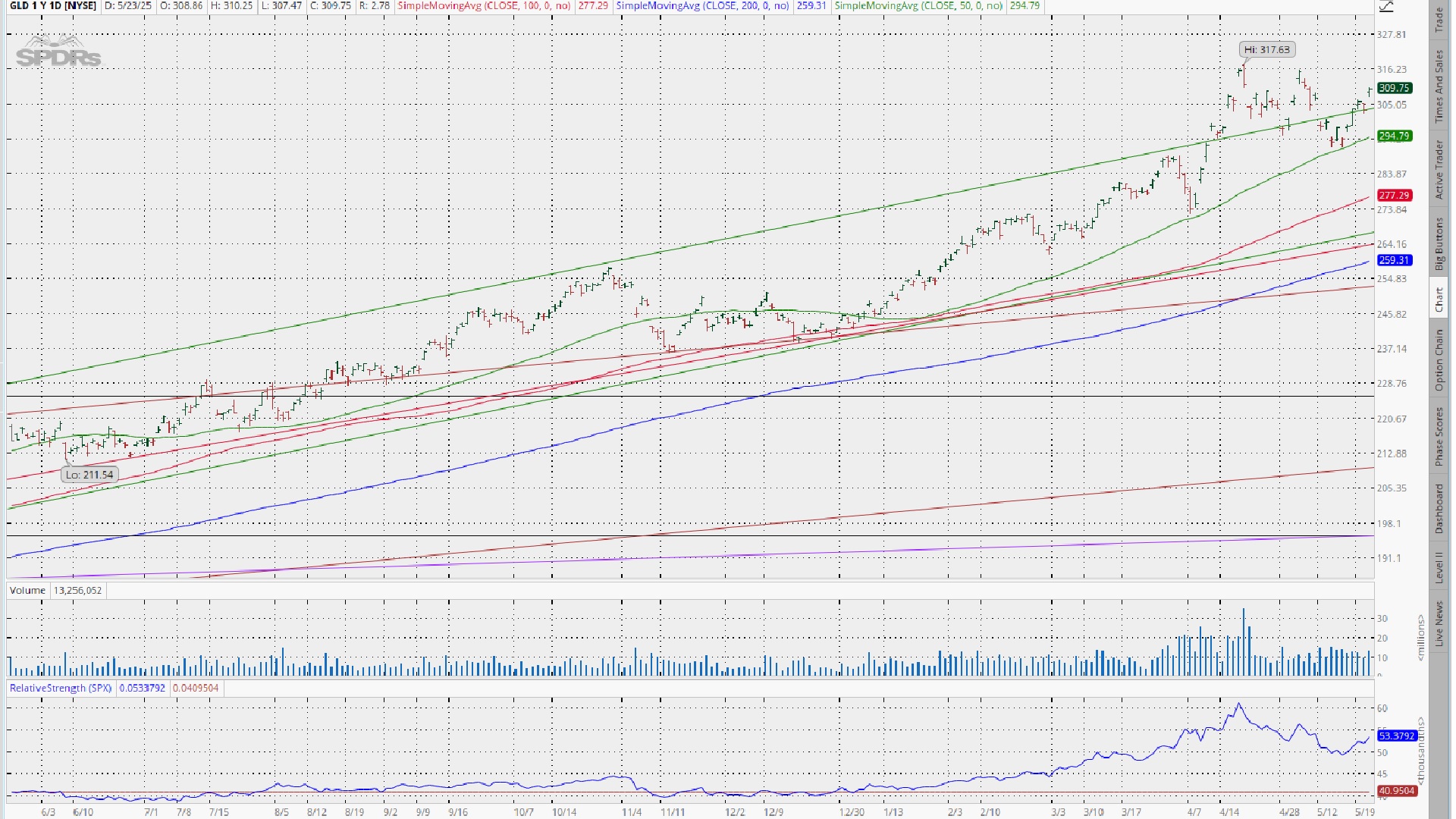

GLD performed pretty much as expected given the

tariff and budget news---bouncing off its 50 DMA and rallying nicely on the week.

Near term, I would expect it to continue to react inversely with bond and stock

markets (i.e., rally off a further deterioration in fiscal policy). It

remains well within a very short term uptrend and in uptrends across all other

time frames as well as above all DMAs. ……stay with what works.

Unsurprisingly, the dollar followed the same

playbook as the rest of the indices---which is to say it got hammered. So for the

moment, the assumption remains that it is heading lower.

Friday in the charts.

Friday in the technical stats.

https://www.barchart.com/stocks/momentum

https://www.barchart.com/stocks/sectors/sectors-heat-map

Fundamental

Headlines

The Economy

The US stats last week were mixed as were the

primary indicators (one plus, one minus). Ditto, the international numbers. So,

no real reason here to contemplate altering my forecast---a ‘muddle through’ economy.

I noted last week that the caveat to this outlook was

that we can’t dismiss entirely the risk of another nuclear

blast coming out of the White House that would again raise the odds of

recession.

And, of course, we got one on Friday when Trump made

a new set of threats against Apple and the EU for not bending to his will. If

this follows what has become the standard script, the parties will have a conversation,

kiss and make up and this will be another of those ‘much to do about nothing’

incidents.

That said, the almost continuous state of

uncertainty fostered by Trump’s trade policy is likely having an impact on businesses

willingness to make long term investment decisions which almost certainly has a

dampening effect on economic growth---hence, recession remains a risk.

To make matters worse/more uncertain, the bond vigilantes

apparently woke up to the fact that fiscal profligacy reigns supreme both here

and abroad---apparently triggered by the house’s passage of the Big, Beautiful

Bill. The Japanese and US bond market were especially hard hit.

What is most concerning is prospect that the

markets have finally reached the end of their patience with the budgetary malpractice

of the ruling class and are about to impose the kind of discipline (refusal to

buy) that will make for a very rough ride in the securities markets.

And.

https://www.capitalspectator.com/inflation-anxiety-and-the-big-beautiful-bill/

I am not making that my forecast---yet. But I am pushing

the yellow warning light. Unfortunately, if this is a false alarm and it doesn’t

lead to a change in fiscal policy, the impact will be all that more painful

when it finally does occur.

Bottom line. Short term, the odds of recession, in

my opinion, remain low. Longer term, the inflation outlook is more visible and getting

worse.

US

International

Other

The death of the penny (speaking of

inflation---which I wish I weren’t).

https://politicalcalculations.blogspot.com/2025/05/the-day-penny-died.html

A deep dive into the housing market.

https://bonddad.blogspot.com/2025/05/new-home-sales-make-3-year-high-as.html

Fiscal Policy

Regime

uncertainty versus market uncertainty.

https://thedailyeconomy.org/article/regime-uncertainty-and-market-uncertainty/

Tariffs

The

negative impact of tariffs on earnings.

https://www.apolloacademy.com/the-negative-impact-of-tariffs-on-earnings/

And now for some good news. Trump endorses

Nippon Steel/US Steel deal.

https://www.zerohedge.com/markets/trump-endorses-us-steel-nippon-deal

Investing

Big oil just went big AI.

The anchoring problem and how to solve it.

News on Stocks in Our Portfolios

What I am reading today

Visit Investing for Survival’s website (http://investingforsurvival.com/home)

to learn more about our Investment Strategy, Prices Disciplines and Subscriber

Service.

Friday, May 23, 2025

The Morning Call---Hedge funds piling into risk off bets

The Morning Call

5/23/25

The

Market

Technical

Thursday in the

charts.

Thursday in the technical

stats.

https://www.barchart.com/stocks/momentum

https://www.barchart.com/stocks/sectors/sectors-heat-map

The latest from Goldman.

Fundamental

Headlines

The

Economy

US

April building permits declined 4.0% versus expectations

of -4.7%.

April existing home sales fell 0.5% versus forecasts

of +0.7%.

https://mishtalk.com/economics/existing-homes-sales-drop-0-5-percent-in-may-but-supply-soars/

The May Kansas

City Fed manufacturing index came in at -10 versus projections of -1.

The May flash

manufacturing PMI was 52.3 versus estimates of 50.1; the May flash services PMI

was 52.3 versus 50.8; the May flash composite PMI was 52.1 versus 50.4.

International

Final Q1 German GDP growth was +0.4% versus

predictions of +0.2%.

April UK retail sales

rose 1.2% versus consensus of +0.2%; the May consumer confidence index was -20

versus -22.

April Japanese CPI

was +0.1% versus expectations of +0.2%.

Other

Overnight

News

Futures plunge on Trump tariff threats.

Fiscal

Policy

Trump tariff/tax

policies losing war with the bond market. Bear in mind that the author of this

piece is a liberal. So the tone is clearly anti-Trump. Unfortunately, much of her

analysis is correct.

The bond market warns Trump/congress of the dangers

of the rising deficit.

A more positive take on the outlook for interest

rates/bond prices.

https://www.zerohedge.com/markets/time-add-duration

Recession

A significant headwind to consumer spending.

https://www.apolloacademy.com/significant-headwinds-to-consumer-spending/

Unsustainable interest rates.

https://dollarcollapse.com/john-rubino-recession-watch-unsustainable-interest-rates/

Investing

Upending asset

allocations.

https://www.wellington.com/en-us/institutional/insights/the-dollar-smile-theory

Are we at a sovereign trust checkpoint?

Why the Japanese bond market is imploding.

https://www.zerohedge.com/markets/why-japanese-bond-market-imploding-goldman-explains

Political CEOs

hurt stock prices.

https://politicalcalculations.blogspot.com/2025/05/political-ceos-hurt-stock-prices.html

Chinese gold

imports surge.

Hedge funds piling into risk off bets.

https://www.zerohedge.com/markets/macro-hedge-funds-have-piled-big-risk-bets

News on Stocks in Our Portfolios

Home Depot (NYSE:HD) declared $2.30/share quarterly dividend, in line with previous.

What

I am reading today

Visit Investing

for Survival’s website (http://investingforsurvival.com/home)

to learn more about our Investment Strategy, Prices Disciplines and Subscriber

Service.

Thursday, May 22, 2025

The Morning Call--The Japanese government bond liquidity crisis is a global warning.

The Morning Call

5/22/25

The

Market

Technical

Wednesday in the

charts.

Wednesday in the

technical stats.

https://www.barchart.com/stocks/momentum

https://www.barchart.com/stocks/sectors/sectors-heat-map

The real move is

hiding in plan sight.

Update on

sentiment.

https://econbrowser.com/archives/2025/05/sentiment-confidence-news

Shorting is hot

again.

https://www.ft.com/content/deecb2a2-04a3-40cf-b835-577b2879d719

Q1 hedge fund

monitor.

https://www.zerohedge.com/markets/hedge-fund-trend-monitor-q1-short-interest-soars-6-year-high

Macro storm clouds

gather.

https://www.zerohedge.com/the-market-ear/markets-pause-macro-storm-clouds-gather

Fundamental

Headlines

The

Economy

US

Weekly initial jobless claims totaled 227,000

versus consensus of 230,000.

The April Chicago

Fed national activity index came in at -.25 versus expectations of -.20.

International

The May German

flash manufacturing PMI was 48.8 versus estimates of 48.9; the May flash services

PMI was 47.2 versus 49.5; the May flash composite PMI was 48.6 versus 50.4; the

May EU flash manufacturing PMI was 49.4 versus 49.3; the May flash services PMI

was 48.9 versus 50.3; the May flash composite PMI was 49.5 versus 50.7; the May

UK flash manufacturing PMI was 45.1 versus 46.0; the May flash services PMI was

50.2 versus 50.0; the May flash composite PMI was 49.4 versus 49.3.

The May German business

climate index was 87.5 versus projections of 87.4; the May current conditions

index was 86.1 versus 86.8.

The May UK industrial

trades orders index was -30 versus forecasts of -25.

Other

Ten risks to the US economy.

https://www.apolloacademy.com/10-downside-risks-to-the-us-economic-outlook/

Update on consumer credit.

Fiscal

Policy

House passes Big, Beautiful Bill.

https://www.zerohedge.com/political/trumps-big-beautiful-bill-narrowly-passes-house-215-214-vote

The reason we should be worried about the

deficit.

A

reason not to worry (Note, the author ignores the impact on inflation).

Lance Roberts isn’t worried.

https://www.advisorperspectives.com/commentaries/2025/05/21/moodys-debt-downgrade-matter-does

However, don’t ignore what is happening in

Japan.

But the ten year Treasury will decide who is

right and who is wrong.

https://www.capitalspectator.com/markets-still-expect-fed-to-keep-rates-steady-for-near-term/

And right now, it is not amused. (See

Wednesday in the charts---above)

https://bonddad.blogspot.com/2025/05/the-bond-market-is-not-amused-on.html

So maybe we should be worried.

Tariffs

An economic lesson from Daivd Ricardo.

https://www.ft.com/content/9e5b5b77-df41-4215-a512-51e04d0aad65

Investing

Japanese government bond liquidity crisis is

a global warning.

https://www.zerohedge.com/markets/price-rice-jgb-liquidity-crisis-global-warning

Innovation and

stock market bubbles.

https://mailchi.mp/verdadcap/innovation-and-stock-market-bubbles?e=513c9c4eac

Outlook for May

dividends.

https://politicalcalculations.blogspot.com/2025/05/the-outlook-for-s-500-dividends-in-may.html

At what interest rate do stocks care?

https://www.zerohedge.com/markets/10y-yields-surge-what-rate-do-stocks-break

News on Stocks in Our Portfolios

What

I am reading today

Visit Investing

for Survival’s website (http://investingforsurvival.com/home)

to learn more about our Investment Strategy, Prices Disciplines and Subscriber

Service.

Subscribe to:

Comments (Atom)