5/26/25

I

am off on a two and half week vacation in Europe. Be back on 6/16. Enjoy your

Memorial Day weekend.

The Market

Technical

Not a great week for the S&P. Between the

latest Trump tariff tantrum and the disappointedly, fiscally irresponsible Big,

Beautiful Bill, neither stock nor bond investors were very happy. The index

ended the week having broken the uptrend off its April 7th low and

hanging precariously above its 100 and 200 DMAs. The only thing to do now is

see whether the S&P will regain that uptrend or reset those two DMAs. If

the latter, then the next visible support level is the 50 DMA (~5584). Follow

through.

As I noted above, the long bond didn’t fare any

better than the S&P. It pushed through (1) the lower boundary of its very short

term trading range---resetting it to a downtrend and (2) the lower boundary of

its intermediate term downtrend. That leaves TLT in downtrends across all time frames

and below all DMAs. If the bond vigilantes are getting serious about refusing to

go along with these spendthrift morons in the ruling class, expect more

downside.

https://www.zerohedge.com/the-market-ear/end-era-8-incredible-charts-bond-markets

Watch the Japanese long bond.

https://www.zerohedge.com/the-market-ear/want-know-where-markets-go-next-watch-japans-long-bond

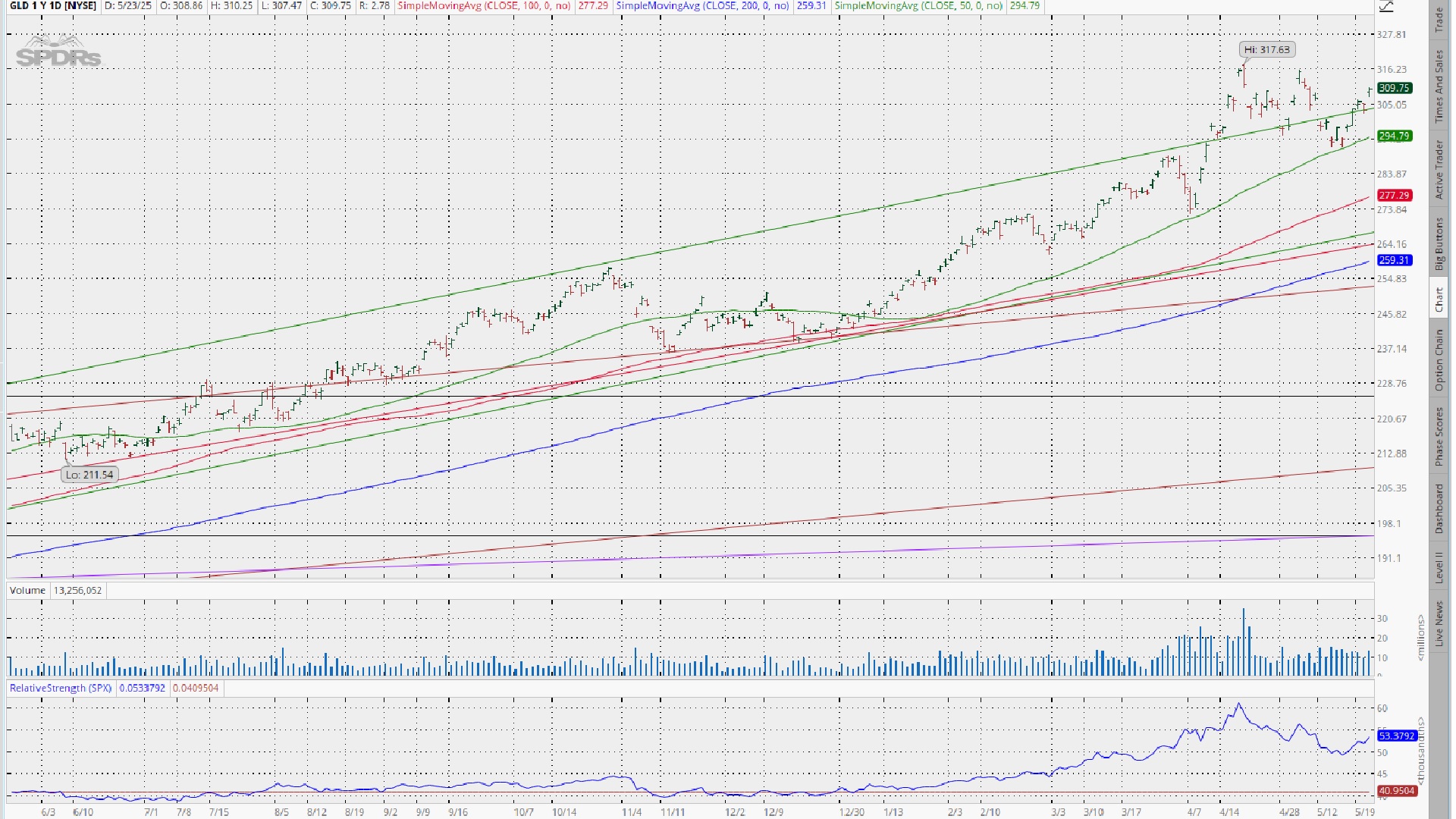

GLD performed pretty much as expected given the

tariff and budget news---bouncing off its 50 DMA and rallying nicely on the week.

Near term, I would expect it to continue to react inversely with bond and stock

markets (i.e., rally off a further deterioration in fiscal policy). It

remains well within a very short term uptrend and in uptrends across all other

time frames as well as above all DMAs. ……stay with what works.

Unsurprisingly, the dollar followed the same

playbook as the rest of the indices---which is to say it got hammered. So for the

moment, the assumption remains that it is heading lower.

Friday in the charts.

Friday in the technical stats.

https://www.barchart.com/stocks/momentum

https://www.barchart.com/stocks/sectors/sectors-heat-map

Fundamental

Headlines

The Economy

The US stats last week were mixed as were the

primary indicators (one plus, one minus). Ditto, the international numbers. So,

no real reason here to contemplate altering my forecast---a ‘muddle through’ economy.

I noted last week that the caveat to this outlook was

that we can’t dismiss entirely the risk of another nuclear

blast coming out of the White House that would again raise the odds of

recession.

And, of course, we got one on Friday when Trump made

a new set of threats against Apple and the EU for not bending to his will. If

this follows what has become the standard script, the parties will have a conversation,

kiss and make up and this will be another of those ‘much to do about nothing’

incidents.

That said, the almost continuous state of

uncertainty fostered by Trump’s trade policy is likely having an impact on businesses

willingness to make long term investment decisions which almost certainly has a

dampening effect on economic growth---hence, recession remains a risk.

To make matters worse/more uncertain, the bond vigilantes

apparently woke up to the fact that fiscal profligacy reigns supreme both here

and abroad---apparently triggered by the house’s passage of the Big, Beautiful

Bill. The Japanese and US bond market were especially hard hit.

What is most concerning is prospect that the

markets have finally reached the end of their patience with the budgetary malpractice

of the ruling class and are about to impose the kind of discipline (refusal to

buy) that will make for a very rough ride in the securities markets.

And.

https://www.capitalspectator.com/inflation-anxiety-and-the-big-beautiful-bill/

I am not making that my forecast---yet. But I am pushing

the yellow warning light. Unfortunately, if this is a false alarm and it doesn’t

lead to a change in fiscal policy, the impact will be all that more painful

when it finally does occur.

Bottom line. Short term, the odds of recession, in

my opinion, remain low. Longer term, the inflation outlook is more visible and getting

worse.

US

International

Other

The death of the penny (speaking of

inflation---which I wish I weren’t).

https://politicalcalculations.blogspot.com/2025/05/the-day-penny-died.html

A deep dive into the housing market.

https://bonddad.blogspot.com/2025/05/new-home-sales-make-3-year-high-as.html

Fiscal Policy

Regime

uncertainty versus market uncertainty.

https://thedailyeconomy.org/article/regime-uncertainty-and-market-uncertainty/

Tariffs

The

negative impact of tariffs on earnings.

https://www.apolloacademy.com/the-negative-impact-of-tariffs-on-earnings/

And now for some good news. Trump endorses

Nippon Steel/US Steel deal.

https://www.zerohedge.com/markets/trump-endorses-us-steel-nippon-deal

Investing

Big oil just went big AI.

The anchoring problem and how to solve it.

News on Stocks in Our Portfolios

What I am reading today

Visit Investing for Survival’s website (http://investingforsurvival.com/home)

to learn more about our Investment Strategy, Prices Disciplines and Subscriber

Service.

No comments:

Post a Comment