The Morning Call

6/25/26

The

Market

Technical

Wednesday in the

charts.

Summary:

A small rebound in Korea sparked a knee-jerk bid in US

equities at the cash open, buoyed by tumbling oil prices. But the bounce

died around the EU close with Nasdaq leading the charge lower into MU

EPS. The dollar continues to surge, weighing on precious metals

and bitcoin was triple-fisted by tech's pain, MSTR perp's

collapse, and the greenback's gain. A lot of volatility today across all

markets amidst a backdrop of falling rates alongside a very weak May

New Home Sales report and an ongoing decline in oil prices as the

Strait of Hormuz continues to reopen to shipping traffic.Rates markets were

perhaps the standout mover today, starting to play catch-down to oil's recent

declines, but equities remain in a world of their own (the wrong way this

time)...

Wednesday in the

technical stats.

https://www.barchart.com/stocks/momentum

https://www.barchart.com/stocks/market-performance

https://www.barchart.com/stocks/sectors/rankings

https://www.barchart.com/stocks/signals/new-recommendations

Is this sell off a

healthy sign?

Counterpoint.

The latest from

Goldman’s flows guru.

Summary:

it is important to note that investor sentiment remains relatively balanced

even as portfolios become increasingly levered to the AI trade. AAII US

Investor Sentiment Bullish Readings Index currently sits at 36 (below ytd

avg and well off ytd high)... Additionally, Goldman’s

US Equity Sentiment Indicator stands at +0.3, the lowest level since

early April... The stock market absorbed >$115b of paper in less than a 2 week

period without blinking. The retail community has been a consistent

buyer of stocks all year – and SpaceX appears to have accelerated the retail

bid. My gut is this trend continues over the remainder of the year. Market

Tailwind.On the retail point, 33b shares traded across all US equity exchanges

last Thursday (6/18 - rebal + SPCX) which was good for the most

shares traded on a single day in the history of the US stock market

(breaking previous record of 30b shares on 4/9/25 AKA Liberation Day).Russell

Rebal this Friday (6/26) will also be an explosive trading volume session.

Buckle Up.There is a noteworthy technical market headwind early next week

as we estimate -$30b of US equities for sale attached to quarter end pension

rebalancing. $30bn to sell ranks in the 89th percentile amongst all buy and

sell estimates in absolute dollar value over the past three years and in the

95th percentile going back to Jan 2000.Heading into SPCX there were concerns

that the long only community would sell sleeves of their portfolios to make

room for new paper.On our trading desk we did not see noteworthy funding

trades from assets managers or SWFs. We saw some trading around the edges but

there was no palpable scramble to raise cash ahead of the deal. MFs are

currently sitting on ~$170b of cash which is inline with their historical

average (from a notional perspective). There is still plenty of dry powder out

there. Yes, even after record deals from GOOGL and SPCX.

Gold isn’t trading

like gold anymore.

https://www.zerohedge.com/the-market-ear/gold-isnt-trading-gold-anymore

Thursday morning

setup: Global stocks and S&P futures are higher while Nasdaq futures are on

a tear after Micron’s sales forecast blew the lights out, brushing aside

fears over a near-term pullback in the AI trade, while Qualcomm set

aggressive targets at its investor day in New York. As of 8:00am ET, a revival

of the AI demand theme is sending contracts on the Nasdaq 100 up 2.1% while

S&P 500 futures are up a more modest 0.7%. MU is +18% pre-market, pushing

Semis higher (SOXX +5%, DRAM +12%) while Mag7 - the companies which

enable all this chip spending - are mostly lower. As Goldman's Delta 1

desks asks, how much longer will they be willing to see their stock languish

while funding semiconductor outperformance? Korea's KOSPI rallied 5.5%

overnight (closing well off the highs) and remains ~2.4% below pre-Flash Crash

levels. While the AI theme is bid pre-market, this is not an ‘Everything Rally’

with Cyclicals seeing a mixed performance with Banks flat, Regional

Banks lower, Energy down with crude, Discretionary mixed, and Materials

flat. Within Defensives, Staples are weaker, HC mixed, and AI-related

Utils names are higher. Brent crude dropped 1.4% to below $73 a barrel, erasing

all Iran war gains, on fears of a supply glut following a ramp-up in

flows through the Strait of Hormuz. Bond yields are flat to +2bp as the yield

curve steepens, but the USD starts the session lower for the first time in 6

sessions. US economic data calendar includes May personal income/spending, 1Q

GDP revision, May durable goods orders, weekly jobless claims and May Chicago

Fed national activity index (8:30am) and June Kansas City Fed manufacturing

activity (11am). Fed speaker slate includes Bowman (8:45am), Goolsbee

(2pm, 6:30pm) and Williams (3:40pm).

Fundamental

Headlines

The

Economy

US

Q1 (final) GDP growth was

+2.1% versus estimates of 1.6%.

Weekly jobless claims totaled 215,000 versus predictions

of 225,000.

May

new home sales fell 7.3% versus consensus of +2.9%; May building

permits declined 0.9% versus -0.7%.

https://bonddad.blogspot.com/2026/06/may-new-home-sales-another-poor-month.html

May PCE index was +0.4%

versus expectations of +0.5%; the core PCE index was up 0.3%, in line.

May

durable goods order fell 4.5%, in line; ex transportation

they were up 1.3% versus forecasts of +0.6%.

May personal income rose 0.7% versus projections of +0.4%; personal

spending was up 0.7% versus +0.1%.

The May Chicago national activity index was reported at -0.1 versus

estimates of +0.12.

International

The April Japanese

leading economic indicators came in at 116.1 versus predictions of 115.9.

The July German consumer

confidence index was -29.2 versus consensus of -27.1.

Other

Overnight

News

Brent erased its

wartime gains as flows through the Strait of Hormuz accelerated. But tensions

remained as Donald Trump warned that tolls in the waterway are a red line issue

in negotiations with Iran.

Iraq will consider

all available options if its OPEC quota is not significantly increased and has

weighed leaving the producer group, sources with knowledge of Iraqi oil policy

told Reuters. The prospect of OPEC's second-largest producer considering an

exit would be a further blow to the group after the departure this year of the

United Arab Emirates. Iraq is one of the five founding members of OPEC, which

was formed in the Iraqi capital.

The BOJ needs to

raise interest rates every few months toward a neutral level of around 2%,

board member Naoki Tamura said.

The EU’s trade

deal with the US is set to go into effect after the bloc gave its final

sign-off ahead of Trump’s deadline. BBG

Iran

There is no agreement on the issue of tolls.

Paying Iran to open the Strait of Hormuz.

https://www.powerlineblog.com/archives/2026/06/easy-mullah.php

Hormuz closure strands 1200 cargo ships.

https://www.ft.com/content/4d3dd2b7-cb6b-410b-8c15-203904f32294?syn-25a6b1a6=1

Summary:

The closure of the Strait of Hormuz has stranded more than 1,200 cargo ships

carrying goods worth an estimated $125bn, according to new data, demonstrating

the vulnerability of global commerce to a handful of strategic maritime

chokepoints. Please use the sharing Justus Heinrich, head of marine

underwriting at Allianz, told the FT the closure of the strait had changed the

perception of risk in chokepoints for insurers. “We were always talking about

realistic disaster scenarios, and now we have a real disaster scenario like

this one,” he said. “So I think it changes a bit the perception of actual

operational risks from ‘it can theoretically happen’ to what we know now out of

this situation.”

Oil tanker rates soar.

Monetary

Policy

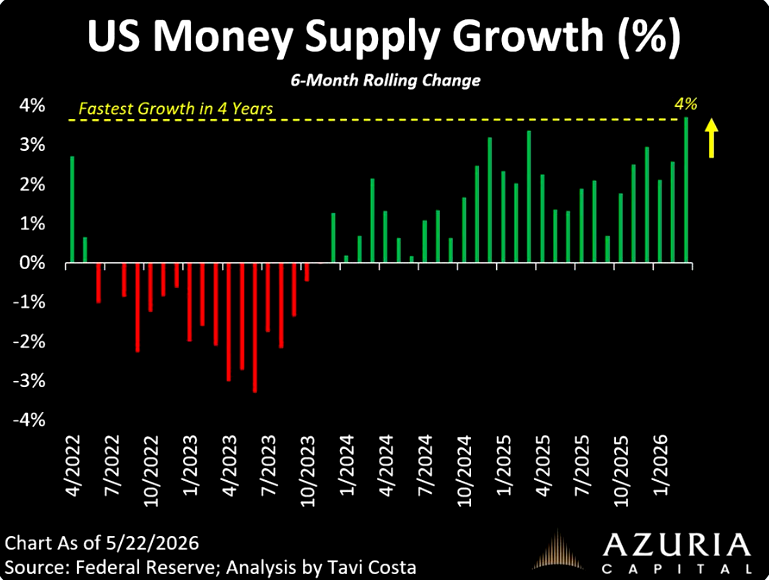

Is

Warsh really a hawk? M2 says no.

https://www.zerohedge.com/the-market-ear/liquidity-crime-scene-follow-money

Summary.

We are currently seeing the fastest growth in US money supply in four years. The

Fed’s balance sheet rose +$11 billion in the week ending June 17th, to $6.74

trillion, the highest since March 2025. Total assets have risen +$162.8 billion

since the start of the year.

The

Financial System

Hedge fund shorting private credit.

Summary: Hedge fund

manager Lee Robinson is shorting insurers, including Lincoln National Corp. and

MetLife Inc., due to their exposure to private credit. Robinson's firm, Altana,

is launching a new fund to protect against a potential downturn in private

credit and its impact on corporate valuations. Insurers' exposure to private

credit has grown significantly over the last decade, with a fifth of the US

life insurance sector's fixed-income holdings allocated to illiquid assets,

mostly private credit, at the end of 2025.

The stocks of private equity/debt managers are

starting to crack.

https://talkmarkets.com/article/alts-continue-to-struggle-1782324910

Investing

Six investment lessons

from a successful fund manager.

https://www.morningstar.com/funds/6-investment-lessons-will-danoff-fidelity-contrafund

Nine lessons from

Jesse Livermore.

https://www.zerohedge.com/markets/jesse-livermore-old-lessons-todays-markets

The cost of

rolling a pretax retirement fund into a Roth IRA.

https://politicalcalculations.blogspot.com/2026/06/the-cost-of-rolling-pre-tax-retirement.html

How to survive the

wrong turns in life and the Market.

https://www.safalniveshak.com/how-to-survive-the-wrong-turns-in-life-and-the-markets/

Warsh hammers

gold.

News on Stocks in Our Portfolios

What

I am reading today

Visit Investing

for Survival’s website (http://investingforsurvival.com/home)

to learn more about our Investment Strategy, Prices Disciplines and Subscriber

Service.

No comments:

Post a Comment