The Morning Call

6/30/26

The

Market

Technical

Monday in the

charts.

Summary:

Dip-buyers filled their boots with big-tech bouncing today after

last week's record

selling with Nasdaq leading the charge (0-DTE faded the initial

move then squeezed to cover). Bonds and the dollar did nothing as oil

rallied (tit-for-tat strikes and no talks). Bitcoin up (choppy) but

gold down. After last week's shitshow, and amid a holiday-shortened summer

week's low liquidity, Nasdaq led the charge today with a dramatic rebound.

Small Caps lagged but all the US Majors closed green on the day... Goldman Sachs' traders noted

that investors paused their demand for pick-and-shovel

(components/chips) and re-engaging with hyperscalers and Software

along for the ride after four straight weekly declines... breadth was so weak... While the S&P 500 P/E has

recently declined, Goldman's Sentiment Indicator of equity investor

positioning rose to 2.0, the highest reading since December 2024... No macro today but higher oil

prices lifted rate-hike odds modestly.. Finally, some potential good

news as the Q2

earnings season is nearly upon us, and AI and hyperscaler capex will remain an

important theme. Notably, the S&P 500 21% return over the past 12

months has been driven entirely by earnings, and Goldman thinks the

combination of a solid macro backdrop plus the ongoing AI investment boom

should lead to another quarter of strong earnings results, despite an elevated

hurdle set by analyst estimates.

Monday in the

technical stats.

https://www.barchart.com/stocks/momentum

https://www.barchart.com/stocks/market-performance

https://www.barchart.com/stocks/sectors/rankings

https://www.barchart.com/stocks/signals/new-recommendations

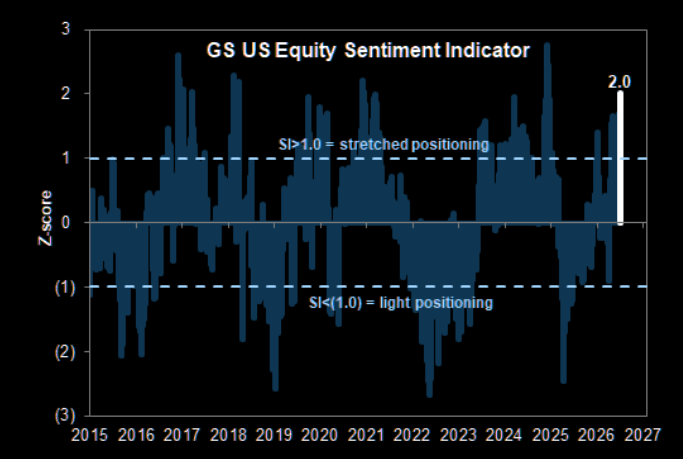

Trillion dollar borrowing binge lifting

stocks to risky levels.

Goldman indicator

most stretched since 2024.

Summary:

GS US Equity Sentiment Indicator of investor positioning is exploding to a

level we have not seen since 2024. What happened? Just as a reminder, here's

what the indicator tracks: "The Sentiment Indicator combines 9 measures

of positioning across institutional, retail, and foreign investors and has

historically been a statistically significant signal for near-term S&P 500

returns."

Source: Goldman

Is oil running out

of sellers?

Tuesday morning

setup: US index futures erased an earlier gain following some belligerent Iran headlines

but are still set to end a quarter that is set to be the S&P

500’s best in six years with markets behaving as though period-end dynamics

have now completed. As of 8:30am, the S&P 500 was flat, pointing

to a calm finish for the index that has surged 14% since the beginning of

April. Nasdaq futures rose 0.1% erasing a sizable gain earlier, but on

pace to close the quarter with a staggering 24% gain; In premarket trading,

semis are mixed, Mag7 are flat, Cyclicals are generally leading Defensives with

exceptions being Energy (lower) and Healthcare (higher). European stocks

rallied, with gains led by Abivax SA after a clinical-trial update soothed investor

concerns. Chipmakers drove Asian shares higher. JPM says with the major US

holiday coming up, keep an eye on low liquidity moves in the region. Bond

yields reversed an earlier drop to trade higher by 1bp pushing the 10Y yield to

4.39%. The USD is stronger, looking to erase all of yesterday’s losses.

Commodities are stronger with crude flat into today’s US / Iran discussions,

Metals seeing a bid, and Ags outperforming the other commodities complexes.

Today's economic data calendar includes April Case-Shiller home prices (9am),

June MNI Chicago PMI (9:45am, several minutes earlier for subscribers), June

consumer confidence and May JOLTS job openings (10am) and June Dallas Fed

services activity (10:30am). Fed speaker slate empty for the session. Chairman

Warsh participates in an ECB panel event on Wednesday in Sintra

Fundamental

Headlines

The

Economy

US

The

June Dallas Fed manufacturing index was reported at 0.0 versus

estimates

of 2.0.

International

Q1 final UK GDP grew

0.6%, in line; Q1 final business investment was up 0.9% versus +0.7%.

The May Japanese

unemployment rate was 2.5%, in line; May industrial

production was up 0.5% versus +1.1%; May YoY housing starts were up

33.9% versus +31.8%; May YoY construction orders

fell 6.9% versus +8.0%.

May German

retail sales rose 1.1% versus expectations of -0.1%; the June unemployment

rate was 6.3%, in line; June CPI fell 0.3% versus unchanged.

The June Chinese

manufacturing PMI came in at 50.3 versus consensus of 50.1; the June services

PMI was 50.2 versus 49.9; the June composite PMI was 50.6 versus 50.7.

Other

Update on alternative business indicators.

Iran

Overnight news.

Shippers pull back amid renewed fighting in

Middle East.

Monetary

Policy

Last

week, I raised the issue of whether the growth in M2 was (1) a precursor to

inflation and (2) a sign the Warsh was really a dove talking hawkish. Lance Roberts elaborates on the issue, pointing

out that (1) the excessive M2 growth in and of itself does not necessarily lead

to future of inflation but (2) can easily lead to it when confronted with a

highly expansionary fiscal policy [which we clearly have]. In my discussion, I also raised the problem

of a restrictive monetary policy (if Warsh is truly a hawk) and an expansive

fiscal policy (which we have had for an extended period of time) which Roberts

addresses in his analysis.

https://www.advisorperspectives.com/commentaries/2026/06/29/friedman-right-mostly-misquoted

Which rules will the Warsh Fed follow?

Summary:

- The Federal Reserve's new chairman, Kevin

Warsh, plans to convene task forces to review the central bank's methods

and operations, including its communications, balance-sheet policy, and

delivery of price stability.

- Warsh has previously frowned on the idea

of relying more on rules to direct monetary policy, such as the Taylor

rule, which ties the policy interest rate to components like inflation and

unemployment.

- Using a rule, such as a nominal GDP rule,

could help organize and discipline the Fed's judgments and explain its

actions to the public, providing a presumption about changes to the policy

rate and calling for an explanation if the Fed decides to do something

else.

Fiscal

Policy

The

Iran war supplemental spending request is wasteful spending.

https://www.cato.org/blog/iran-war-supplemental-rife-wasteful-spending-should-be-rejected

AI

Bank on International Settlements warns of AI

crash.

AI sales start to justify data center spending

boom.

Summary:

Revenue

from artificial intelligence has reached a tipping point, showing that the

hundreds of billions of dollars tech companies are spending on it may be

economically sustainable.

- Global AI sales, excluding China, reached

$25 billion in the first quarter of 2026, exceeding the industry’s

estimated $21 billion in depreciation costs.

- The margin for error is narrow, with

depreciation charges still consuming more than two thirds of revenue,

leaving a small buffer to cover other costs such as power, labor and

financing.

The

Financial System

Private credit is making bets on consumer debt.

Summary: The private

credit industry was dubbed “shadow

banking” as it took business away from traditional lenders. Buy Now, Pay

Later companies have been referred to as hawking “phantom

debt” that falls outside Wall Street’s typical tracking methods.Now, these

two more opaque corners of finance are overlapping in a big way — and catching

the attention of credit raters, former regulatory chiefs and others on guard

for potential risks as US consumers show mounting signs of strain. Officially known as

“forward-flow agreements,” investing heavyweights like Blue Owl Capital

Inc., KKR & Co. and Elliott Investment Management are

increasingly agreeing to pre-purchase billions of dollars worth of loans before

they’re made, in a bet that consumer assets will outpace returns elsewhere.

That’s been a boon to the likes of Klarna Group Plc, Affirm Holdings

Inc. and PayPal Holdings Inc., offering fuel for the origination machines

at the heart of a business more Americans are embracing. Skeptics are anxious

the model incentivizes churning out more loans to consumers, with some drawing

parallels to the lead up to the subprime mortgage crisis where

originate-to-sell practices detached risk from reward. But participants counter

that originators can retain chunks of the loans they sell — a structure that

reassures private credit buyers who see these short-term consumer assets as a

way to diversify their billions of dollars of longer-term financing agreements.

This much is clear: The strategy is at the intersection of two industries

navigating their own challenges.

Investing

Wall Street’s $270

billion speculation machine.

https://www.zerohedge.com/markets/ai-rout-exposes-wall-streets-270-billion-speculation-machine

Summary:

On the surface, the week’s casualties appeared unrelated. In reality, they

belonged to the same corner of modern markets: products built to let investors

express the hottest trade with more leverage, less friction and greater

frequency. That’s become one of the defining features of this bull market.

Every winning narrative now spawns an expanding ecosystem of investment

products built around the same idea, from leveraged ETFs and options to

digital-asset derivatives and prediction markets. They differ in structure, but

all promise investors a faster, more concentrated or more leveraged way to own

the market’s hottest trade. The category has grown rapidly. Leveraged

ETFs, which use derivatives to deliver multiples of an asset’s daily return,

now oversee more than $270 billion in assets globally, with the US accounting

for more than $200 billion and Asia exceeding $45 billion, according to data

compiled by Bloomberg. As their assets have grown, the funds have become a

bigger source of forced buying and selling, potentially amplifying moves in the

stocks and indexes they track. Barclays estimates rebalancing by US leveraged

ETFs has recently surged to several times its long-term average, creating

mechanical buying and selling flows potentially large enough to influence

broader market trading. Christopher Getter, a portfolio manager at Simplify

Asset Management, says the growing menu of speculative funds can make it easier

to bet on complex companies without fully understanding them. SpaceX, for

example, is valued at levels that assume years of future growth, while its

limited public float and anticipated index inclusion have created technical

forces that can overwhelm traditional valuation metrics.

Be careful of

quantum computing.

https://www.riskhedge.com/outplacement/do-not-be-a-raccoon

The case for value over growth in building.

https://www.apollo.com/wealth/the-daily-spark/the-case-for-value-over-growth

The Market narrative is changing.

https://www.apollo.com/wealth/the-daily-spark/the-narrative-in-markets-is-changing

Burying your head in the sand is not the best

advice.

https://www.tker.co/p/investors-should-not-ignore-forget-unsettling-events

Why are investors holding more cash?

https://awealthofcommonsense.com/2026/06/why-are-investors-holding-more-cash/

Prices still know the future.

https://alphaarchitect.com/impressive-markets-hypothesis/

Crowded trades are not always bubbles.

News on Stocks in Our Portfolios

What

I am reading today

Robotic warfare is shifting the source of

state power.

https://letter.palladiummag.com/p/war-by-other-means

Freedom isn’t just

another word.

https://www.wsj.com/opinion/freedom-isnt-just-another-word-806a54f8

Visit Investing for Survival’s website (http://investingforsurvival.com/home) to learn more about our Investment

Strategy, Prices Disciplines and Subscriber Service.