The Morning Call

6/24/26

The

Market

Technical

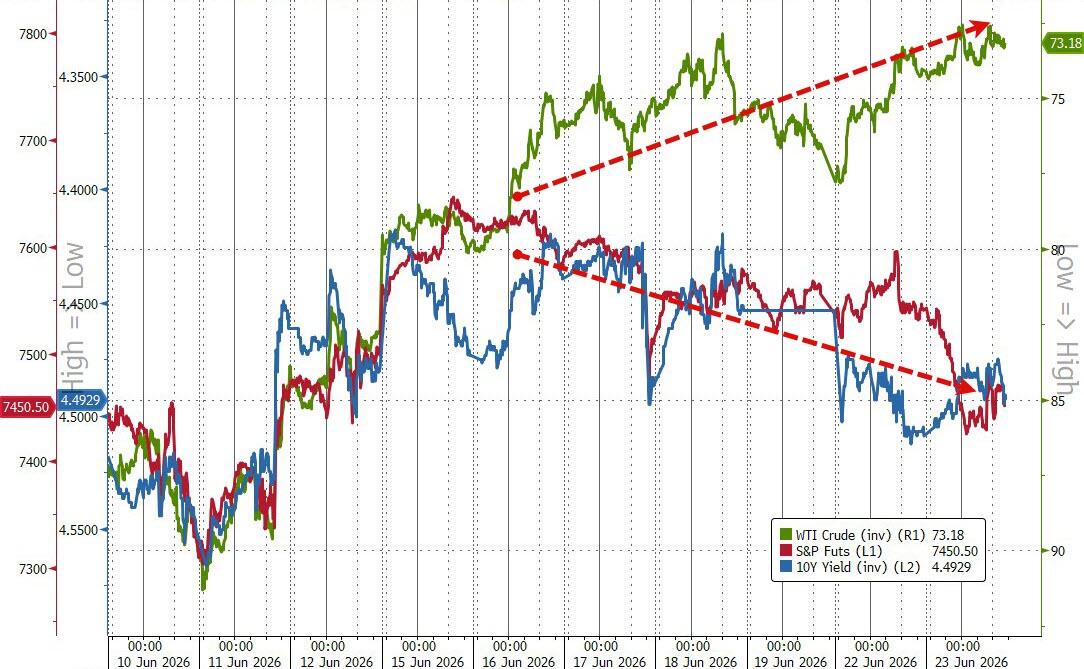

Tuesday in the

charts.

https://www.zerohedge.com/markets/us-tech-trounced-bonds-bid-korean-butterfly-flaps-its-wings

Summary:

Oil oscillations took a back seat to Korean carnage today as the flapping

of levered ETF butterflies triggered a tornado in US big-tech (led by

Semis), dragging down Nasdaq (Dow green though). Heavy

negative delta 0-DTE flow today. Bonds (mixed macro) and the dollar

were bid as Bitcoin and bullion were dumped again. The question

on everyone's lips: Are levered Korean retail traders the US Tech

boom Giant killer? It was a soft-data tsunami today (and the picture was

anything but clear): Philly Fed Services ugly (and contracting), Richmond Fed

Manufacturing and Business Conditions ugly (and contracting), but US Composite

PMI jumped to 5 month highs led by Manufacturing (at 49-month highs) amid signs

of price pressures cooling. ADP's weekly employment indicator remains near its

highs though as labor remains resilient. Still, it continues to be NOT about

macro as stocks and bonds decouple from any head- or tail-wind from oil...

Finally, Apollo's Chief Economist, Torsten Slok, lays

out the top three macro questions for traders at the moment:

1) Middle East: What are the

implications if some tanks reach critical levels somewhere in the world,

including distillate fuels in the US?

2) AI: What happens if companies start

limiting their token budgets meaningfully because they are only seeing weak

ROI, and as a result, compute demand either slows down or shifts to Chinese

models?

3) Inflation outlook: With inflation

trending higher, what are the implications for equity and credit markets if the

Fed hikes in September and December, as currently priced in fed funds

futures?

The answer in all these

cases is not straightforward but we would say that the market remains

more than willing to look past all these potential pitfalls... until now. Is

this week's decline a canary in the coalmine? And will Korea's flapping

butterfly wings chaotically trigger a global delivering in the chase for

bottlenecks?

And

just to rub some salt in that wound, buybacks ain't gonna save you this

time (and not just because hyperscalers FCF is negative):

Tuesday in the

technical stats.

https://www.barchart.com/stocks/momentum

https://www.barchart.com/stocks/market-performance

https://www.barchart.com/stocks/sectors/rankings

https://www.barchart.com/stocks/signals/new-recommendations

The AI trade is

getting uncomfortable.

https://www.zerohedge.com/the-market-ear/ai-trade-getting-uncomfortable

Summary:

The AI trade is starting to look crowded in all the right places and vulnerable

in all the wrong ones. Tech volatility is exploding, systematic flow risks are

building and the market continues to reward the suppliers while punishing the

spenders. Nothing is broken yet, but the rubber bands are getting stretched. The

market continues to reward AI suppliers while punishing AI spenders. Semis,

memory and infrastructure have captured the upside, while hyperscalers face

growing questions around returns and capex intensity.Meanwhile, increasingly

capable models are emerging from the East at a fraction of the training cost

incurred by Western AI leaders. Yet the entire AI ecosystem remains priced for

ever-rising capex. Nobody is positioned for "slightly less." The

figures are starting to get uncomfortable. Projected selling from

options-related flows, leveraged ETFs and vol-control funds is becoming

absolutely massive.

How far can the

rubber band get stretched?

Summary:

The breaking point was always likely to be when one of the major spenders

concludes that shareholder returns are better served by spending slightly less.

The problem is that “slightly less” is not embedded in anyone’s

assumptions.The entire AI complex is priced for ever rising capex as

inference demand grows. The Nasdaq appears to have failed to make a

decisive new high.At the same time, there are increasingly visible issues

surrounding the largest market-cap companies in the world.That feels like an

unstable equilibrium.

We

are through the tailwinds of last week’s expiry and now have line of sight into

month-end and quarter-end rebalancing flows, which in theory should

favor selling equities and buying bonds. Market structure is also becoming less

supportive.Dealer gamma is lower around current spot levels and declines

further on the way down.CTAs are still buyers on many measures but remain

highly convex to the downside. A glance at the prime brokerage numbers

largely confirms what price action is telling us: the world has

become one exceptionally concentrated trade.AI is driving the

equity market, the equity market is driving economic expectations, and all

roads increasingly lead back to the same handful of stocks. Risk that the

market has been ignoring the highly deflationary forces in token economics.

Wednesday morning setup;

US stocks are set for a rebound with equity futures higher as Semis and Tech

stage a partial recovery from yesterday’s "Chip-Wreck" as KOSPI

retraced about 20% of its losses ahead of earnings from the single-biggest

contributor to US outperformance this year: Micron’s third-quarter numbers are

an even bigger deal than usual, following Tuesday’s shakeout of an overcrowded

AI trade that’s has been priced for perfection. As of 8:00am ET, S&P

500 futures are 0.3% higher with Nasdaq 100 contracts up 0.5%. In premarket

trading, equities are boosted by a bid for Semis (MU +3.6% with earnings

tonight) with most of Mag7 higher. Within Cyclicals, Discretionary and

Industrials are the standouts as Energy / Fins are mostly lower. Cyclicals

poised to lead Defensives with Momentum factor flat. Bond yields are lower

1-2bp as the yield curve flattens, pushing 10Y yields; USD remains bid even as

real yields decline. DXY set a new 52-wk high today. Cmdty remain under

pressure dragged by the Energy complex and weakness in Metals. Today’s macro

data focus is on Home Sales ahead of tomorrow's update on GDP, PCE, Personal

Income / Spending, Cap / Durable Goods, and weekly Claims.

Fundamental

Headlines

The

Economy

US

Weekly mortgage

applications rose 1.0% while purchase applications declined 1.0%.

Month

to date retail chain store sales were up 10.0% versus +9.4% in the prior week.

https://bonddad.blogspot.com/2026/06/consumer-spending-has-turned-red-hot.html

The June flash manufacturing

PMI was 55.7 versus estimates of 54.5; the flash services PMI was 51.3 versus

51.0; the flash composite PMI was 52.2 versus 50.8

The

June Richmond Fed manufacturing index was 4 versus expectations of 9.

International

The June German

business climate index came in at 85.6, in line; the June current conditions

index was 87.0 versus 86.4.

Other

Overnight

News

The US Senate

voted 50-48 to pass a resolution to halt the Iran war unless US President Trump

gets approval from Congress. However, the White House said Congress resolutions

on Iran are non-binding and won't be sent to President Trump, while Trump criticized

the Senate passage of the Iran war powers resolution, which he claimed provides

aid and comfort for the enemy.

The BoJ sees the

risk of inflation exceeding its 2% target and will conduct additional

interest-rate hikes appropriately, Governor Kazuo Ueda said in speech Wednesday

that reiterated policymakers’ recent messaging

Iran

The first tango in

Lake Lucerne. https://x.com/JoshBlockDC/status/2069047098813690054?ref_src=twsrc%5Etfw%7Ctwcamp%5Etweetembed%7Ctwterm%5E2069047098813690054%7Ctwgr%5E0924bdd8e9caa093d89c2e70ad43737050772d7e%7Ctwcon%5Es1_c10&ref_url=https%3A%2F%2Fwww.powerlineblog.com%2Farchives%2F2026%2F06%2Ffirst-tango-at-lake-lucerne.php

Ukraine, Iran and Occam’s Razor.

https://danieldrezner.substack.com/p/ukraine-iraq-and-occams-razor

Monetary

Policy

Real Treasury

yields rise above 2%. Is the Market

doing the Fed’s job? (if it is, that is good news since the Fed has done a

horrible job)

https://www.capitalspectator.com/real-yields-rise-above-2-is-the-market-doing-the-feds-job/

Fiscal

Policy

Debt hawks ignore history.

The

Financial System

Apollo caps private credit fund withdrawals.

Summary:

Apollo

Debt Solutions, which has roughly $25 billion in assets, capped withdrawals

at 5% of outstanding shares on Monday after investors asked to redeem 16.8%,

according to a shareholder letter. Redemption requests in the quarter were

higher than the 11.2% investors wanted to pull in the prior period. Cliffwater

LLC faced requests to pull 17% of shares from its flagship fund, while BlackRock

Inc. received about 13% earlier this month. Both funds enforced a 5% cap for

such funds, known as business development companies.

Investing

Can tech stocks

keep outperforming?

https://alhambrapartners.com/weekly-market-pulse-markets-review/?src=news

This analyst thinks

they can.

https://www.riskhedge.com/outplacement/the-biggest-ai-investing-mistake

Tech companies

getting money while the getting is good.

The end of cheap capital.

https://hbr.org/2026/06/the-end-of-cheap-capital

The S&P’s

latest changes in its composition.

https://www.carsongroup.com/insights/blog/the-sp-500s-latest-changes-ai-in-consumer-out/

How much of the

S&P 500’s revenues come from overseas?

https://talkmarkets.com/article/how-much-of-the-sp-500s-revenue-comes-from-overseas-1782232562

Spotting bubbles

and calling tops.

https://awealthofcommonsense.com/2026/06/spotting-bubbles-and-calling-tops/

News on Stocks in Our Portfolios

What

I am reading today

Visit Investing

for Survival’s website (http://investingforsurvival.com/home)

to learn more about our Investment Strategy, Prices Disciplines and Subscriber

Service.

No comments:

Post a Comment