The Morning Call

7/21/26

The

Market

Technical

Monday in the

charts.

Summary:

Amid a quiet macro week, investors are bracing for the micro (mega-cap

earnings) and after OpEx unclenched Gamma, markets were freer to

move today (Nasdaq higher, rest lower). Bitcoin bounced alongside

big-tech and bond yields jumped despite oil prices well off their highs

chopping around unch, (fuel products higher). The dollar and

gold went nowhere. The loss of positive dealer gamma after July options

expiration leaves the S&P 500 less pinned, according to Bloomberg

macro strategist, Michael Ball, giving any momentum rally greater scope to

pull the broader market higher.Weakness in semiconductors and other crowded

AI-infrastructure winners has pushed high-beta momentum into one of its fastest

and deepest drawdowns on record. But the size of the recent drawdown in past

AI-winners and more negative positioning does indicate there is a risk

of a squeeze higher, which was the case on Friday. Broader market

positioning matters more now.

Monday in the

technical stats.

https://www.barchart.com/stocks/momentum

https://www.barchart.com/stocks/market-performance

https://www.barchart.com/stocks/sectors/rankings

https://www.barchart.com/stocks/signals/new-recommendations

Margin debt jumps

(again) in June.

https://www.advisorperspectives.com/dshort/updates/2026/07/20/margin-debt-finra-june-2026

The dollar signals

a continuation of its bearish chart pattern.

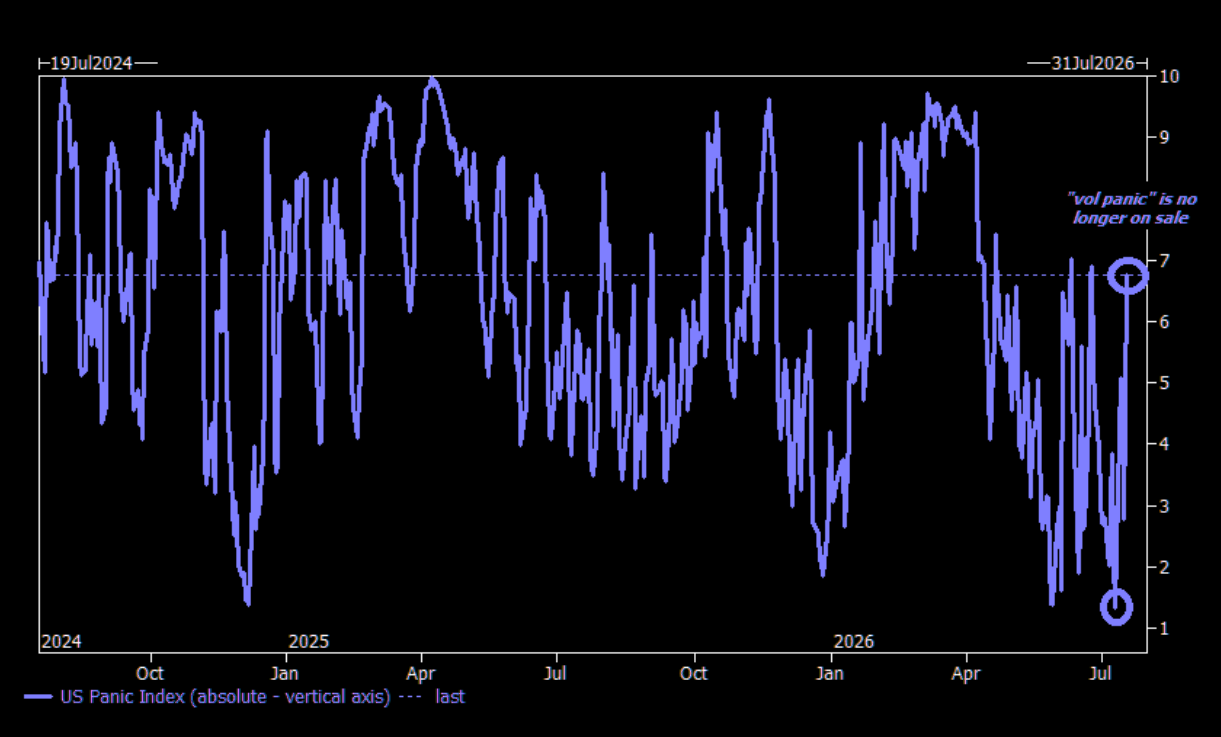

The VIX isn’t

telling the whole story.

https://www.zerohedge.com/the-market-ear/calm-storm-vix-isnt-telling-whole-story

Summary:

The VIX still looks remarkably calm. Beneath the surface, however, the picture

is very different. Single-stock volatility has exploded, semiconductors are

swinging wildly, dealer gamma has deteriorated and investors are increasingly

paying for downside protection. Goldman's volatility

panic index has surged in recent sessions. Unlike the VIX, it captures a

broader set of volatility signals, offering a deeper read on market stress.

What happens after

a 20% drawdown in the semis?

https://www.zerohedge.com/the-market-ear/what-normally-happens-after-20-drawdown-semis

Summary:

15 episodes of >20% drawdowns in SOX over the past 15 years. 5 turned into

>30%. Worst 44%. What happens after a 20% drawdown? 20 days later = 8%

positive return. On average.

Tuesday morning

setup: US stock futures are higher led by Tech after a strong bounce in chip

stocks in Japan (memory stock Kioxia traded limit up after trading limit down

on Friday and Monday was a holiday) and Korea, as evidence mounts that Momentum

/ Semis pullback have bottomed, with supportive price action elsewhere in Asia

and Europe, though the JPM EU Trading Desk is not yet seeing follow-through

buying in Semis. As of 7:20am ET, S&P futures are 0.5% higher,

lagging the 1.4% bounce in Nasdaq futures helped by a report that TSMC

is planning price hikes, although it is unclear if the early ramp will

persist amid the re-escalating war with Iran which overnight saw Houthis impose

a blockade on Saudi Arabia. In premarket trading, most Mag 7 names are higher

with semis leading (SOXX +4%). Cyclicals ex-Energy are leading Defensives with

both Staples and HC net lower and AI boosting Industrials and Utils. WTI crude

is trading near its highs, boosting Energy as all 3 commodity complexes move

higher with silver the standout which has traded in tandem with the AI theme.

The yield curve is twisting steeper with yields ranging from -1bp to +1bp with

USD flat. Today’s macro focus is on the weekly ADP number and regional Fed

activity. US economic data calendar includes ADP weekly employment

change (8:15am) and July Philadelphia Fed non-manufacturing index (8:30 am).

Fed speaker slate is blank during July 18-30 external communications blackout

period around the July 28-29 FOMC meeting.

Fundamental

Headlines

The

Economy

US

International

The May UK

unemployment rate was 4.9% versus consensus of 5.0%; May average earnings were

up 4.3% versus +4.5%.

The

July EU economic sentiment index came in at 23.4 versus predictions of 11.2;

the July German economic sentiment index was 26.3 versus 18.0; the July German

current conditions index was -77.1 versus -77.8.

Other

Crude oil versus refined product prices.

https://econbrowser.com/archives/2026/07/eyes-on-refined-product-prices

This analyst believes

oil prices will remain elevated through the end of 2027.

https://talkmarkets.com/article/interview-with-christiane-baumeister-oil-price-shocks-1784561347

The manufacturing sector of the economy

continues to improve.

https://bonddad.blogspot.com/2026/07/the-manufacturing-sector-of-economy.html

Overnight

News

President Trump is

nearing a decisive fork in the Iran war, with U.S. and Israeli officials

envisioning only two viable endgames: Option 1: Pursue a new 10-day ceasefire

aimed at reopening the Strait of Hormuz. Option 2: Launch a massive joint

military campaign with Israel to force Tehran's capitulation.

OpenAI and

Anthropic executives are sounding the alarm about the rise of cheap AI,

particularly powerful new models produced in China, suggesting they will lead

to a “dystopian” AI future and present unacceptable security risks without

regulation.

The cost of

protecting Oracle Corp.’s debt against default reached a fresh multi-year high

on Monday while its existing bonds sold off, as doubts grew over whether the

company’s massive investments in artificial intelligence will pay off.

Iran

Overnight news.

Inflation

Gold is the constant. What it signals is in substantial decline.

Confusion over how

the Fed/Warsh is measuring inflation. Lost in this somewhat esoteric struggle

to define inflation is the fact that however the Fed has defined inflation,

they have never met the goal anyway. I

am a whole lot less concerned about defining inflation than I am about the Fed

having the balls to manage monetary policy to meet the whatever its definition

is.

https://stayathomemacro.substack.com/p/2-of-what

What

the yield curve is telling us about inflation.

Inflation

conundrums.

https://www.advisorperspectives.com/commentaries/2026/07/20/conundrums-inflation

A statistical revamp is about to lower

inflation.

Tariffs

Trump slams Canada with 50% tariff on selected

goods.

The

Financial System

They are doing it again.

(4)

Oh My Fucking God, They're Doing It Again

Investing

Why retail traders consistently

underperform.

https://www.advisorperspectives.com/commentaries/2026/07/20/why-retail-traders-underperform

News on Stocks in Our Portfolios

What

I am reading today

A

look at the future of warfare.

Visit Investing

for Survival’s website (http://investingforsurvival.com/home)

to learn more about our Investment Strategy, Prices Disciplines and Subscriber

Service.