4/22/24

The Market

Technical

It was another punk week for the S&P. It reverted its 50 DMA from support to resistance

and appears to be about to challenge its 100 DMA (now ~4931). Still not enough

to prompt a great deal of worry, but….we need to be aware of potential downside

(i.e., support levels). Those exist at ~4674 (the 200 DMA) and ~4436 (the lower

boundary of its short term uptrend). The good news is that the S&P has now

filled that gap up open and remains above multiple support levels. The bad news

is that those multiple support levels exist at much lower levels. It is too

soon to be committing cash.

Tech titans: a bounce and then a

move down?

https://www.zerohedge.com/the-market-ear/tech-titans-bounce-now-and-then-next-move-down

The long bond’s rough ride continued, putting in

another gap down open on Monday (there are now three of them). It now (1) is below

all DMAs (2) has made four lower highs and

will likely make a fifth barring a substantial rally and (3) is in downtrends

across all time frames. Unless you like trying to guess bottoms, this is no

time to buy bonds.

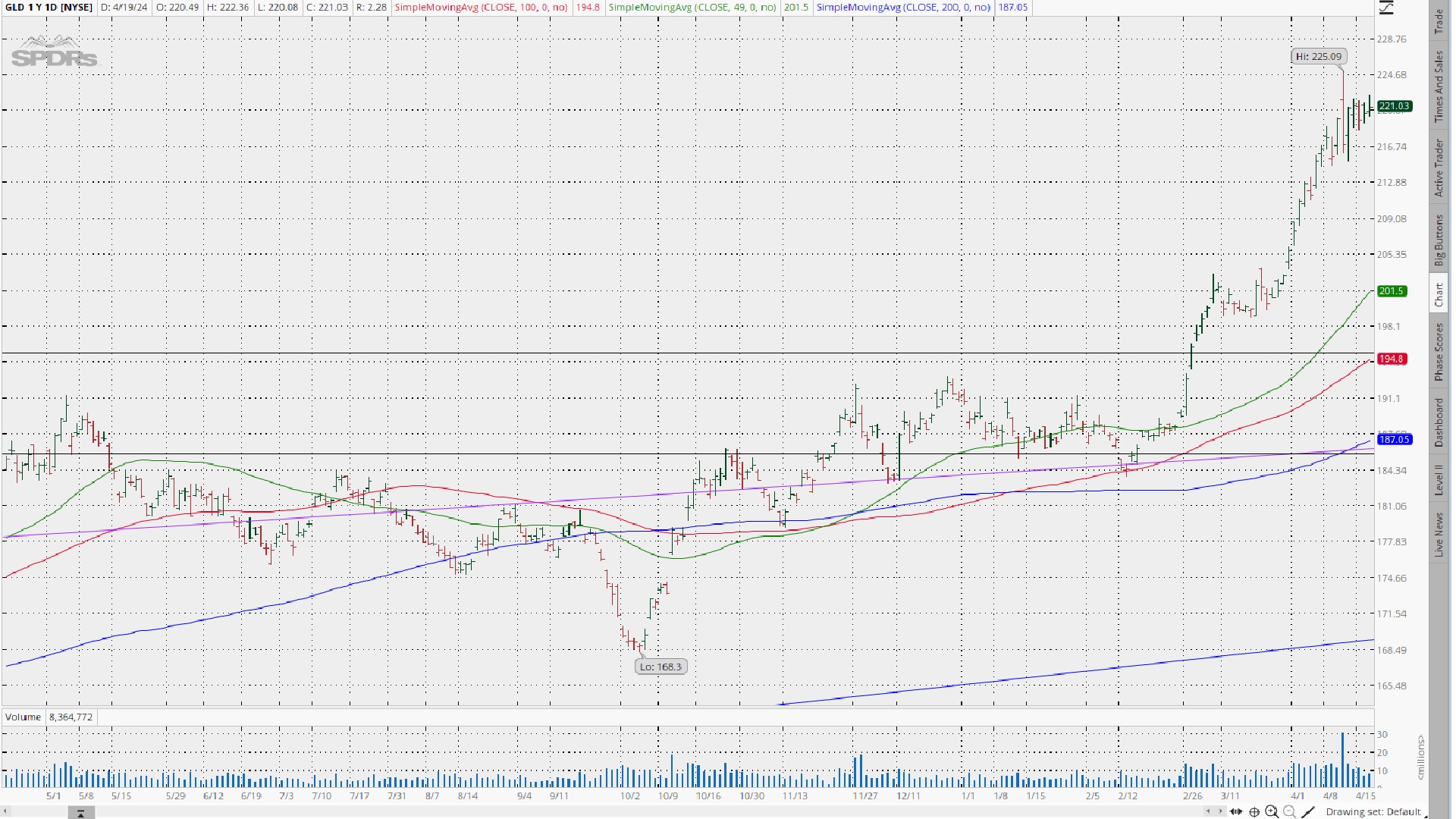

GLD maintained its upward momentum though at a

vastly reduced pace. That makes sense given fears of inflation (of which I continue

to become more convinced) and geopolitical turmoil.

I continue to hold my GDX (gold miners ETF).

The dollar had a flattish week, though it did

confirm its successful challenge of its 200 DMA (now support). I remain somewhat puzzled by the dollar’s strong

performance viz a viz the pin action in the long bonds and gold. On the other

hand, those two huge gap up opens suggest future weakness which would bring it more

in line with the rest of the indicators.

Friday in the charts.

https://www.zerohedge.com/markets/tech-wrecks-fedspeak-fks-fomo-followers-gold-hits-new-record-high

Fundamental

Headlines

The Economy

Week

in review

Last week’s stats were slightly weighted to the

negative side with one primary indicator positive, one neutral and three

negative. Despite the headline narrative that the economy is gaining strength,

the numbers just aren’t there. On the other hand, there is nothing in the

overall data to indicate a recession.

I noted last week that I was starting to believe

that we may be returning to the pre-covid ‘muddle through’ economy. The more I think

about it, the more sense that makes, especially given that the main tenant that

of forecast (i.e., too much government debt usurping private capital/resources)

is even worse today. As a result, I am a short hair away from revising my outlook

from recession to ‘muddle through.’

The inflation data continues to make for unhappy

investor reading. The result being that I changed my forecast to one in which

inflation is and will likely remain a problem. And that fits well with the

above notion of excessive government spending/debt. Adding that to a

historically dovish Fed (its current hawkish noises, notwithstanding) and the

recent performance of commodities (gold, oil) and bitcoin leads me to the

conclusion that inflation may be as good (low) as it is going to get.

Those hawkish Fed noises.

But my favorite optimist still believes inflation

is declining.

https://scottgrannis.blogspot.com/2024/04/belated-march-cpi-analysis.html

Bottom line:

(1)

as long as the government pursues its current

spend, spend policy, I don’t see us making any further progress in lowering the

inflation rate. Indeed, the Fed’s hawkish rhetoric aside, I don’t think it has

any choice but to continue monetizing the government IOUs.

(2) the question of

recession [what kind of landing] remains a bit murky, but I think that the

economy has shown enough strength to warrant modifying my recession forecast

slightly to a ‘muddle through’ scenario. I am not quite there; but another week

or so of inconclusive stats and I will be.

US

The Chicago national activity index came in at .15

versus estimates of .09.

International

Other

Fiscal Policy

Five

fiscal truths (must read).

https://www.cato.org/blog/five-fiscal-truths

Ruling

class suckers.

Debt

to GDP ratios around the world.

https://www.zerohedge.com/economics/how-debt-gdp-ratios-have-changed-around-world-2000

Recession

Update on big four recession indicators.

Commercial real estate foreclosures soar.

War in the Middle East

While most pundits are rejoicing over Israel’s

rather contained response to Iran’s missile attacks on the Jewish homeland in

the hopes that a serious war has been avoided, Mohamed El Erian is not so sure.

https://www.ft.com/content/53f64b6b-3151-46b3-ad83-3a4732c35d41

Bottom line.

The latest from BofA. (must read)

How well does a ‘buy and hold’ strategy work?

https://www.hunterlewisllc.com/insights/how-bad-could-it-get

The indispensability

of risk.

https://www.advisorperspectives.com/commentaries/2024/04/19/indispensability-of-risk-howard-marks

News on Stocks in Our Portfolios

What I am reading today

Visit Investing for Survival’s website (http://investingforsurvival.com/home) to learn more about our Investment

Strategy, Prices Disciplines and Subscriber Service.

No comments:

Post a Comment