The Morning Call

5/4/26

The

Market

Technical

There is just no quit in this Market. The S&P was up for the week, making a

fourth gap up open on Friday. The technicals remain ‘full steam ahead’ with the

S&P (1) making another new all-time high, (2) above all three DMAs and (3)

in uptrends across all timeframes. The technical question in my mind is how long

can this sprint higher last without a correction?---coupled with the more

fundamental question of the economic impact (growth and inflation) of the war

(destruction of the Middle East oil infrastructure) which is as yet unanswered.

As you know, I approached this upside move

cautiously---which couldn’t have been more wrong. Nonetheless, I am loath to

chase this upswing, especially with (now) four gap up opens

sitting below. The only good news in this trading error is that a number of

stocks on my Buy List have remained within buying parameters. So with any

retreat, I can make a delayed entry.

Should you ‘sell

in May’?

https://www.carsongroup.com/insights/blog/lets-talk-about-sell-in-may/

Goldman warns crash

risk spiking.

Summary:

The clearest implication of narrow breadth for investors is continued Momentum

volatility, which can act as a destabilizer for the market once momentum

reverses. While narrow breadth can persist for months, eventually it resolves

in either a "catch up" or a "catch down” (i.e., meltup of

"everything else" or meltdown of the handful of "market

generals"), with both outcomes consistent with Momentum

volatility. The Goldman strategist warns that the bank's Prime data shows hedge

fund net tilt to Momentum ranks near a multi-year high. In addition,

while hedge fund gross leverage has declined during the last couple weeks, it

remains elevated relative to history, ranking at the upper end of the 5-year

range. In short, the longer this narrow-breadth meltup persists, the

greater the risk of a sharp, violent drawdown (to avoid the

more popular term crash).

TLT was down on

the week and is nearing the lower boundary of its very short term trading

range. And it remains below all DMAs and in downtrends across all major

timeframes. With stagflation the likely result of the

destruction wrought on the oil infrastructure, I am hard pressed to think that

bond prices are going to improve markedly.

Gold reset its 100

DMA to resistance. It remains in a very short term downtrend marked by the top

and now two lower highs. I am watching to see if it makes a second higher low

or continues its downward momentum. The good news is that it (1) remains in

uptrends across all time frames and (2) still has one gap down open overhead

that needs to be filled. I will likely rebuild my GDX position when it breaks

through that very short term downtrend.

Silver on the

verge.

https://www.zerohedge.com/the-market-ear/silver-verge-one-push-away-squeeze

Summary:

Silver just printed its biggest up candle in a while and is pressing against a

large wedge/triangle formation. A close above the 50-day MA (roughly another

dollar) could open the door to a squeeze.

The dollar failed to sustain its upward momentum, could not

challenge its 50 and 200 DMAs (both remain resistance) and now challenging its

100 DMA to the downside. The good news is that it has two gap down opens

overhead that needs to be filled. That said, I continue to believe that the

macroeconomic backdrop of the US economy (slow growth and rising inflation)

suggests a low to lower dollar.

Friday in the

charts.

Summary:

A new day, a new month... and another record high on negative

breadth. With even Goldman

warning that bad things happen when only a handful of high momentum

names carry the entire market (especially to now daily all-time highs)

while most stocks drop, the S&P decided to demonstrate and closed at a

fresh record high on yet another day of brutal negative breadth - this

was the 4th record high of the past 5 that saw way more decliners (328) than

advancers (172)!

Friday in the technical stats.

https://www.barchart.com/stocks/momentum

https://www.barchart.com/stocks/market-performance

https://www.barchart.com/stocks/sectors/rankings

https://www.barchart.com/stocks/signals/new-recommendations

Monday morning

setup: US futures whipsawed and crude oil spiked higher as tensions flared up

again in the Middle East, taking the focus off a run of strong earnings by

megacap tech companies. As of 8:00am ET, S&P and Nasdaq 100 futures dropped

0.2% from Friday's record highs, falling as much as 0.5% just minutes earlier

after Iran’s Fars agency claimed two missiles hit an American patrol

boat, before erasing most of the declines after the US denied a ship was

hit. All of this after Trump said Sunday that US Navy will guide ships

out of the Strait of Hormuz from Hormuz in a move called “Project Freedom"

while Iran issued Trump a one-month deadline for negotiations on its

proposed 14-point deal to reopen the Strait of Hormuz. European stocks were

mostly red while tech-heavy Asia indexes in South Korea and

Taiwan surged in Monday trading. In premarket trading, Mag 7

names are mixed: GOOGL (+0.6%), AMZN (+0.6%), and META (+0.7%) are outperforming,

while AAPL and MSFT are lower. Brent crude surged more than 5% to trade above

$113 a barrel before paring the gain, while bitcoin and gold traded in a mirror

image. Interest rates are higher with the 10Y yield rising 4bps to 4.41%; WTI

crude added ~$2 to $104 this morning having briefly traded above $107; base

metals are higher, while gold and silver both sliding more than 2%. Looking at

the US economic data calendar slate includes March factory orders at 10am. Fed

speaker slate includes New York Fed President John Williams at 12:50pm

Fundamental

Headlines

The

Economy

The

US stats tilted to the positive side last week though the primary indicators

were balanced (five plus, three neutral, five negative) of which there was one

neutral and two negative price reports. Overseas, the data was very

disappointing for a second week in a row although there were two positive and

one neutral inflation readings.

We

still aren’t seeing any economic effects of the Iran war and the turmoil in the

private credit market in the US numbers though perhaps the last two week’s

global data is the first sign---and that makes sense to me especially with

respect to economic growth since it is more heavily dependent oil availability.

On

the other hand, somewhat surprisingly, the inflation data in the US was poor

while overseas the numbers were upbeat. That said, given the ongoing

constrained oil supply and the damage to the global oil producing

infrastructure my guess is that these statistics will only get worse.

Inflation is rocking and rolling.

There

were no new incidents of private credit deterioration. Though clearly that

doesn’t mean that there won’t be. Nonetheless, most of the analysis (which I have

linked to) suggests that while there could be some negative fallout from this

problem, it is unlikely to reach the order of magnitude of the great financial

crisis. In addition, several of the private credit ETFs being bought suggesting

investors are becoming more sanguine.

We

should get some new insights during/following this week’s Milken Conference.

While this all leaves me with heightened concern about both growth and

inflation/stagflation, the stock market is anything but worried. I am not sure

if (1) this is a buy-the

rumor-sell-the-news situation, (2) investors correctly believe that earnings

growth will continue at its current pace irrespective of the damage being done

by the destruction of the Middle East oil infrastructure and I am wrong to be

worried or (3) investors incorrectly believe earnings growth will continue at

its current pace irrespective of the damage being done by the destruction of

the Middle East oil infrastructure I am right to be worried.

Color me clueless. But until the magnitude of the war’s economic impact on

the US economy becomes clearer, my choice is to stay on the sidelines even if I

am proven wrong to be worried.

US

The April final manufacturing PMI was 54.5

versus consensus of 54.0.

https://www.advisorperspectives.com/dshort/updates/2026/05/01/sp-global-manufacturing-pmi-april-2026

The April ISM manufacturing index was 52.7

versus projections of 53.0.

International

The April final EU manufacturing PMI was

52.2, in line.

Other

March median household income.

https://politicalcalculations.blogspot.com/2026/05/median-household-income-in-march-2026.html

Update from my favorite optimist.

http://scottgrannis.blogspot.com/2026/04/m2-update-still-looking-like-inflation.html

Counterpoint.

(3)

13 Week Money Supply Growth is Trending Above 5%

Update from a not so optimistic Econobrowser.

https://econbrowser.com/archives/2026/04/a-worried-econ-watcher

Update on big four recession indicators.

https://www.advisorperspectives.com/dshort/updates/2026/04/30/the-big-four-recession-indicators

Iran

Overnight news.

Monetary

Policy

The

Fed is setting policy off of a partisan mood ring.

Major central banks are cautious.

https://www.zerohedge.com/markets/final-warnings

The

Dollar

Where is the de-dollarization?

Investing

The latest from

BofA.

https://www.zerohedge.com/markets/hartnett-enjoy-boom-loop-event-could-open-door-doom

Summary:

stocks & commodities love nominal booms (long the Cs - commods,

chips, consumer, China), bonds (steeper curve) &

US dollar not so much. Hartnett next look at this week's "tale of the

tape", where understandably the main event is the ongoing “boom

loop” as policymakers counter deglobalization, populism, and

inequality... with max govt spending (up

60% since 2020 and set to rise 15% in proposed FY27 budget), play

geopolitics via inflationary trade, industrial, and financial market policies

to monopolize supply of chips, oil, rare earths, minerals needed to win AI war The

only thing that breaks 2020s boom loop, Hartnett thinks, is bond collapse.

And speaking of a bond

collapse, Hartnett concludes the note with his "The Price is Right"

section, where the BofA strategist says that while 5% is the “Maginot

Line” for 30-year Treasury, he expects it to hold.

The biggest bubble

of modern times.

(3)

Stocks Now In “The Biggest Bubble Of Modern Times”

Why countries are

stocking up on gold.

The permanent distortion theory.

(3)

The Permanent Distortion Theory - by Quoth the Raven

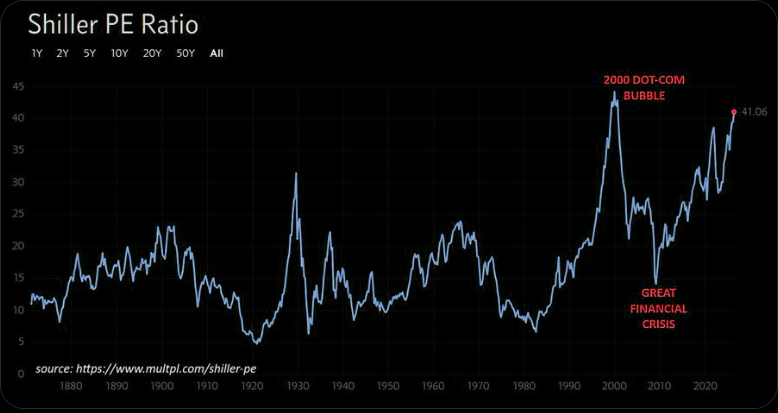

The S&P 500

Shiller PE just hit 41x. The only time it's been higher was December 1999,

right before the dot-com crash.

News on Stocks in Our Portfolios

What

I am reading today

Notes for self-education.

https://jillianhess.substack.com/p/richard-feynmans-notes-for-self-education?ref=thebrowser.com

Visit Investing

for Survival’s website (http://investingforsurvival.com/home)

to learn more about our Investment Strategy, Prices Disciplines and Subscriber

Service.

No comments:

Post a Comment