The Morning Call

2/13/15

I have a number of family

obligations that I have to attend to this weekend; so no Closing Bell. But I have made a brief summary of the points

usually covered in that note.

The Market

Technical

The indices

(DJIA 17972, S&P 2088) lifted nicely yesterday, ending within uptrends

across all timeframes: short term (16588-19364, 1929-2910), intermediate term

(16629-21784, 1753-2467) and long term (5369-18860, 797-2093). The S&P and NASDAQ closed at all-time

highs while the Dow fell short of its mid-December peak (19989). Momentum continues to shift to the upside.

Volume

rose; breadth improved. The VIX declined

10%, finishing within its short term trading range, its intermediate term

downtrend and below its 50 day moving average.

The drop broke the lower boundary of the developing pennant

formation---which if confirmed (at the close today) would be a plus for stocks.

The

latest from Stock Traders’ Almanac: the

pin action around President’s Day (short):

The

long Treasury fell again, but not by much.

It remains within short term, intermediate term and long term uptrends

and above its 50 day moving average. I

continue look for price stability; but it is not happening.

GLD’s

chart gets sicker by the day. While it

did finish within a short term uptrend and an intermediate term trading range,

it is back below its 50 day moving average.

My finger is on the trigger.

Bottom

line: investors’ mood seemed to improve

with better geopolitical events out of Ukraine and the EU/Greek

discussions. Momentum and breadth were

better, though our internal indicator continues to suggest that all is not

well. The Averages are now out of sync

with the S&P hitting at an all-time while the Dow trailed. However, it is well within striking distance;

so this discrepancy can be overcome very quickly. If that occurs, then the upper boundaries of

the indices long term uptrends (18860/2093) will again likely prove difficult

resistance.

The TLT fell

once again, dispelling the notion that it had found some stability in

yesterday’s pin action. My anxiety grows daily in its absence. GLD is a short

hair away from history.

Fundamental

Headlines

Wednesday’s

news flow repeated itself yesterday---poor economic data but positive

geopolitical events. US economic data

included higher than expected weekly jobless claims, really poor January retail

sales and a stunning decline in December business sales. Clearly more cognitive dissonance for our

forecast.

Just

how bad is the current data flow (short):

Overseas,

Sweden lowered its central bank lending rate (more ‘beggar thy neighbor’) and

the third largest Austrian bank announced balance sheet problems resulting from

the revaluation of the Swiss franc---neither likely to be a plus for global

economic growth. On the other hand,

December Japanese machinery orders were quite strong. As always, I will take a positive anywhere I

can get it.

***overnight,

a pleasant surprise---in the fourth quarter, EU GDP grew 0.3%, Germany 0.7% and

France 0.1%. Australia spoiled the party

by reporting the highest unemployment rate in 13 years.

The

good news was that:

(1)

Merkel seems to have defused the Ukrainian turmoil, [a]

providing enhanced autonomy for eastern Ukraine {and Russia’s land bridge to

Crimea}, [b] gaining IMF funding for Ukraine to help with its financial

problems and [c] end running the US dangerous drive for more weapons for

Ukraine and more Russian sanctions. If

this agreement materializes and holds, it would remove a big potential negative

from the global economy as well as investor psychology.

The latest from

Ukraine---it is not the terms (vague), it is the will to implement (medium):

And the US

appears to be walking back on Russian sanctions. We need Putin as a special advisor for US foreign policy

(medium):

(2)

contrary to the Wednesday night rumors of an ‘agreement

in principle’ between the EU and Greece over the resolution of Greece’s

financial problems, it was still clear by Thursday morning that there was

none. Though the parties were engaging

in good faith negotiations. To be sure,

that doesn’t mean that all parties to the discussion are being polite or that a

satisfactory solution can be achieved.

But hope springs eternal; and until the fat lady sings, investors seem

intent on accepting the most upbeat interpretation of ongoing events.

The next official meeting date is Monday 2/16 [our

Presidents’ Day holiday] and that should provide some more detail on the

substance and flexibility of the EU/Greek positions. I caution again about getting too jiggy over

a workable solution being achieved before it actually is.

A less optimistic view (medium):

Germany’s tough choices (medium):

But they are apparently getting

closer (short):

The

latest statement from overnight (short):

Bottom

line: both the US and international

economic data flow continue to point to some softening. However, we can’t dismiss this morning’s

upbeat EU GDP news. This reinforces the recent

change in direction of EU stats towards less bad news; and that is good

news. Like the increased sloppiness in

US numbers, the question is, are the improving EU data noise or a sign of a

shift in direction? Too soon to know; but clearly, this just adds more

uncertainty to our outlook. At the

moment, I am making no revisions to our forecast. I remain hopeful that the US is experiencing

just another one of those periodic hiccups that it has in the past; but the

added burden of a currency devaluation arms race and poor international stats are

making (despite the ray of hope in Europe) that position increasingly difficult to

sustain.

On the other

hand, the two potential nuclear explosions that could derail the global (Ukraine

and Greece) economy appear more likely to be resolved satisfactorily. And that could remove major potential

negatives.

Still, a

sluggish US economy that seems to be underachieving with increased vigor,

hampered by misguided central bank monetary policies and a slowing global

economy is not the best prescription for higher stock valuations when those

valuations are already at or near historic highs.

I

can’t emphasize strongly enough that I believe that the key investment strategy

today is to take advantage of the current high prices to sell any stock that

has been a disappointment or no longer fits your investment criteria and to

trim the holding of any stock that has doubled or more in price.

Bear

in mind, this is not a recommendation to run for the hills. Our Portfolios are still 55-60% invested and

their cash position is a function of individual stocks either hitting their

Sell Half Prices or their underlying company failing to meet the requisite

minimum financial criteria needed for inclusion in our Universe.

Equity

valuations not cheap (medium):

Great

7 minute video starring Jim Bianco on stock valuations:

Thoughts on Investing from Josh Brown

A lot of

new investors assume that managing money is like golf – where Tiger Woods whips

the amateur who steps out on the course with him 100 times out of 100.

But it’s

not like that at all.

In

investing, unlike golf, the amateur can crush the pro for an appreciable period

of time. That’s one of the most wonderful things about the game and one of

the most frustrating things about the game, all at once.

In

addition, the professional golfer gets to keep his trophies and wins regardless

of the subsequent decline in his skills. In contrast, the professional

investor’s average or below-average years will dilute the benefit of his

“winning” years as mean reversion knocks his lifetime track record back down to

earth. Peter Lynch must have known this when he retired in 1990 at the top of

his game – he left the magic intact before reality and probability could strip

him of it.

Randomness

and Time team up to take almost all of us down, one way or the other.

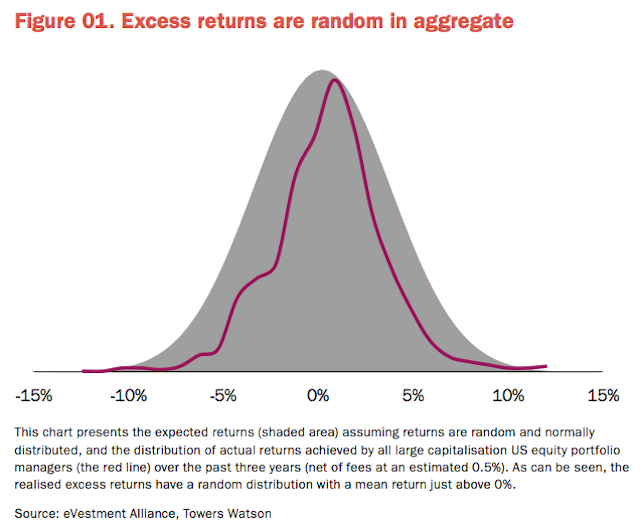

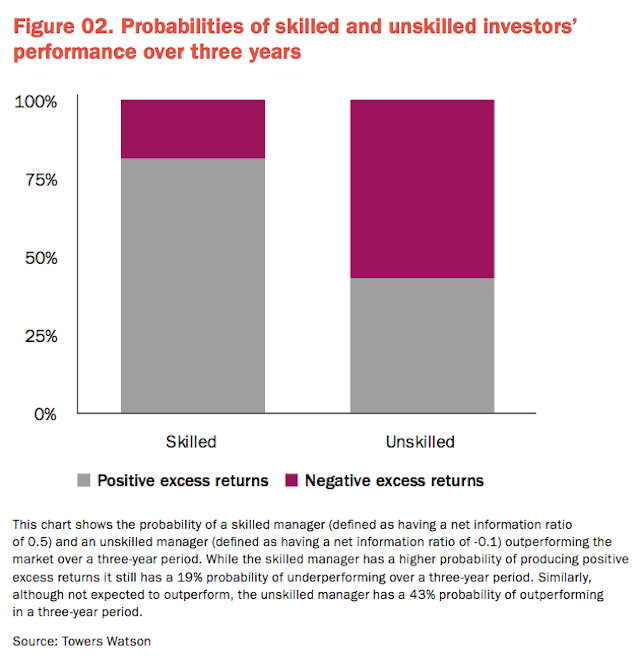

Here are

three charts from a recent presentation from Towers Watson on equity investing

that show this phenomenon graphically (emphasis mine):

Past performance in particular can sound a plausible basis

upon which to form an opinion. This is because we are programmed to recognize

patterns in nature and to extrapolate what we believe we have observed.

However, studies

have shown that there is a high degree of randomness in relative investment

returns and that to be statistically significant, a performance record should

be intact for nearly 15 years. Few investors meet this criterion.

Fewer still meet this requirement and have not experienced other changes which

have a direct impact on future performance, such as staff turnover or growth in

assets under management which can affect portfolio construction. Consequently, we strongly believe that –

considered in isolation – past performance is a poor basis for assessing

investment skill.

Josh here

– in other words…

Excess

returns can show up anywhere, in any portfolio, and are randomly achieved in

aggregate:

Any

schmuck can hang with the pros, for a long time, and beat a skilled investor

for years before his information disadvantage becomes apparent. And the skilled

managers are very capable of underperformance as well, Towers Watson notes that

even Warren Buffett recorded two three-year rolling periods of negative

relative-performance, despite his 45-year marathon track record of outperformance:

And

finally, we are all, in the end, victims of our own success. Identifying a

manager with durable skill and a sustainable investing process only assures one

thing – that others will discover that manager as well and pour their dollars

in. And then, like hearing your favorite indie band on Top 40 Radio, you’re

totally grossed out and uncomfortable. And with good reason – your alpha is now

dust in the wind. Nothing ruins an outperforming investor or an indie rock band

like mass appeal:

After seeing these charts and this evidence of futility,

you might be asking yourself the following: If anyone can win and anyone can

lose at any time in the markets, why

bother trying at all?

Fair question. But I submit to you that successful

investing is a lifetime

pursuit, and in the end, it’s the pursuit itself that offers the rewards

along the way. The destination was never the thing – most of us aren’t meant to

end up as Peter Lynch or Warren Buffett. No, it was what you learned on the way

there that made all the difference. As the poet C.P. Cavafy reminds us:

Ithaka gave you the marvelous journey.

Without her you would not have set out.

Without her you would not have set out.

A lifetime

of outperforming the markets is unattainable for most. But a lifetime of

self-improvement and the acquisition of skill and knowledge – that’s available

for anyone who’s willing to go for it.

News on Stocks in Our Portfolios

o

V.F. (NYSE:VFC):

Q4 EPS of $0.98 in-line.

o

Revenue of $3.58B (+8.8% Y/Y) misses

by $10M.

Economics

This Week’s Data

December

business inventories rose 0.1% versus expectations of up 0.2%; business sales

plunged 0.9%.

Other

The

burden of US government finances (medium and a must read):

Fed

or fundamentals (short):

Politics

Domestic

GOP backtracks

on immigration (medium):

International War Against Radical Islam

Closing Bell Notes

1. The

trend in US economic numbers continues to be disappointing.

2. International

economic numbers were mixed this week with some good numbers out of Europe. The question is, is this noise or a change in

trend?

3. Earnings

season: what started off with potential

negative implications fizzled somewhat in the end. To be sure, fourth quarter final profits will

be less than anticipated but they will be much better than I thought two weeks

ago. The question is still guidance and

we won’t know that for another three months.

For the moment, this is a byline.

4. Oil:

it is still bouncing around in price and there is still no consensus on whether

that is good or bad for the economy/stocks.

5. Vulnerable

banking system: the banksters are back in the headline with a spate of stories

on investigations and subpoenas over misdeeds. In addition, Austria’s third

largest bank is having balance sheet problems resulting from the Swiss franc

revaluation. However, a resolution of the Greek dilemma will ease potential

pressure on balance sheets.

6. Central

bank money printing: Sweden climbed on the money for nothing bandwagon this

week; however, the main news flow focused on the extent of economic weakness in

China and what that might mean for monetary/currency policies. A weakening yuan will not be great for trade

or deflation pressures.

International ramifications of EU QE

(medium):

7. Geopolitical

risks: At the moment, the Ukrainian conflict seems to have been defused but at

the cost of an implicit Russian success.

That is still a plus. Greece is

still talking.

Bottom line:

the trend in the current data flow suggests the risk of slower than expected

growth in the US is mounting, though I am not yet making changes in our

forecast. Better reported profits

prevented this development from becoming worse; and the improved stats out of

Europe raised hope that our ‘muddle through’ scenario is alive and well. Nonetheless, problems exist outside of Europe

leaving the global economy as the biggest negative to our outlook. The impact of lower oil prices still aren’t

apparent except in the oil patch.

The

banksters continue to do their part to weaken investors’ confidence in their

financial viability as the central bankers step up their game of ‘beggar thy

neighbor’.

Resolution

in Ukraine removes a geopolitical risk; we still know nothing on Greece except

that both sides are still talking. This

is not over but the tone has improved.

The

Market technicals improved this week.

The Averages appear to be preparing for another assault on the upper

boundaries of their long term uptrends.

While

the resolution of potentially traumatic geopolitical events reduces the risk of

an air pocket in equity prices, stocks are still way overvalued by virtually

every measure. But history suggests that

any correction will come as a result of some unforeseen event which by

definition is unforeseen.

Take

profits where appropriate, get rid of anything that resembles a loser and learn

to love cash.

No comments:

Post a Comment